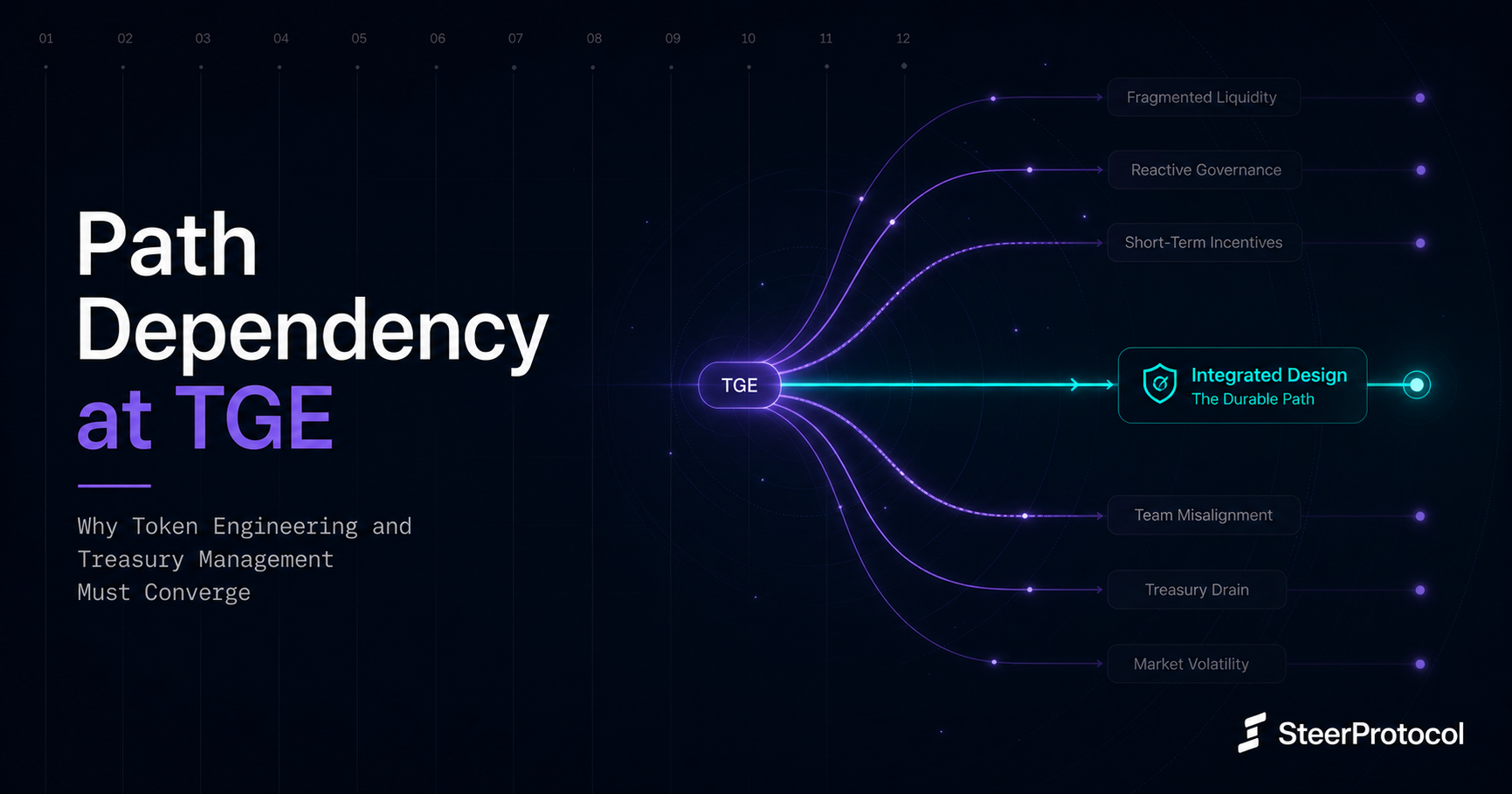

Path Dependency at TGE: Why Token Engineering and Treasury Management Must Converge

A TGE is not just a token distribution event - it is the first market-design decision in a token’s lifecycle. This blog explores why token engineering and treasury management must converge before launch, and how float, liquidity, venue mix, incentives, and treasury strategy shape whether a token becomes merely tradable or evolves into durable, financeable capital.

Most teams still treat TGE as a distribution milestone: finalize supply, set unlocks, secure listings, seed liquidity, turn on incentives, and go live.

That framing is too narrow for today’s DeFi market.

A TGE is not just a token launch. It is a market-design event. The decisions made on day zero — float, venue mix, liquidity placement, market-maker reliance, treasury deployment, incentives, and unlock structure — create a path dependency that shapes everything that follows.

A token’s lifecycle moves through a sequence: market formation, liquidity formation, utility, financialization, control, and longevity. If the launch structure is wrong, each later stage becomes harder to recover. If it is designed correctly, the token has a real path to become more than a traded asset. It can become usable capital, financeable capital, and eventually a durable market system.

That is why token engineering and treasury management can no longer operate as separate workstreams. They must converge before TGE, not after it.

Launch is no longer just distribution

Most teams still approach TGE as if it is mainly a distribution exercise.

Finalize supply. Set unlocks. Secure listings. Seed liquidity. Turn on incentives. Go live.

But that is not how token markets actually form anymore.

DeFi is now large enough that launch design sits much closer to market-structure design than campaign execution. The market is no longer just a place where tokens list and trade. It is a financial system where tokens can become collateral, liquidity primitives, treasury assets, governance instruments, yield-bearing positions, and inputs into broader structured products.

That changes what launch decisions need to account for.

A TGE is not just a token distribution. It is the first market-design decision in the life of an asset.

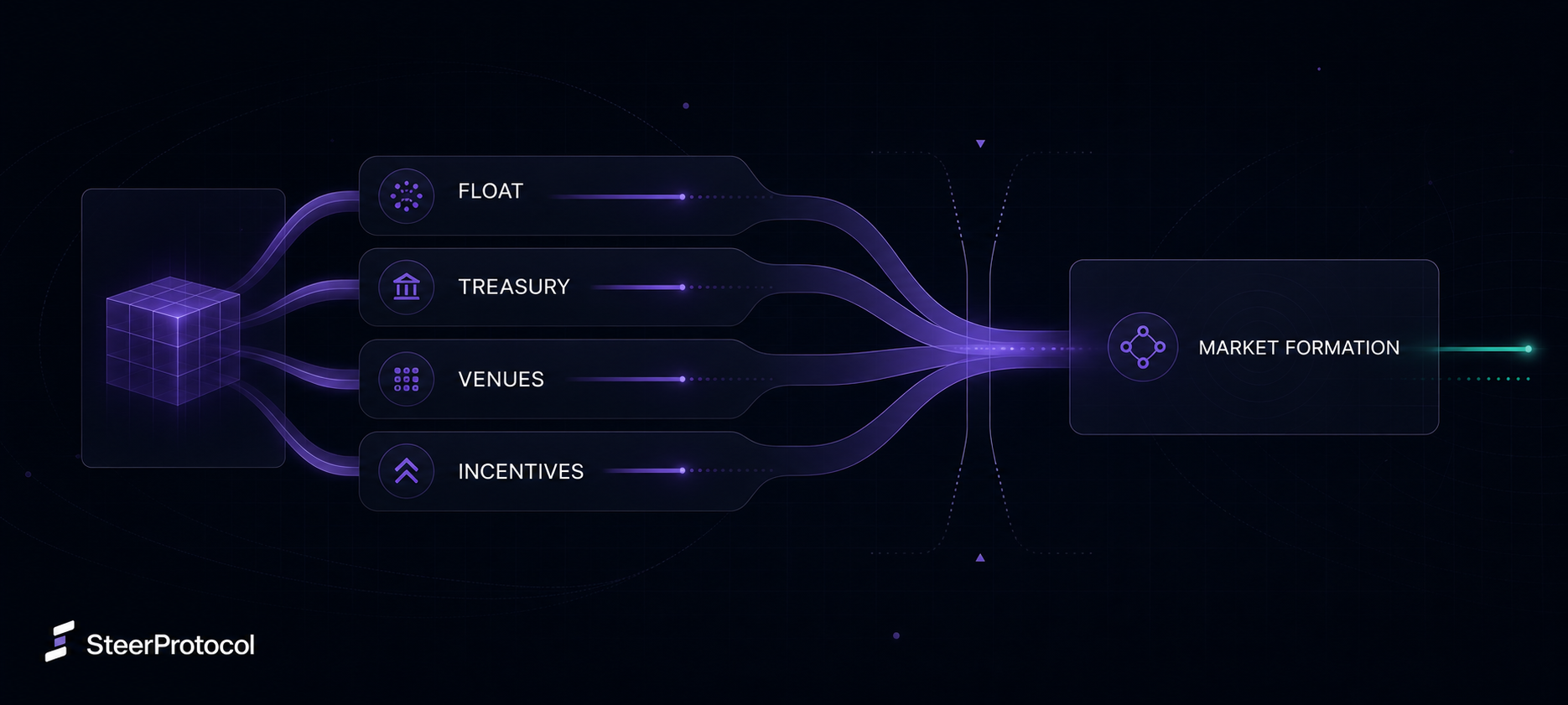

The choices made on day zero — float size, venue mix, market-maker reliance, treasury deployment, liquidity range placement, unlock schedules, and incentive structure — shape the path that follows.

Every token market has to move through the same broad lifecycle:

- Market formation — where price discovery begins.

- Liquidity formation — where depth, execution quality, and volatility absorption emerge.

- Utility — where the token starts being used inside products and protocols.

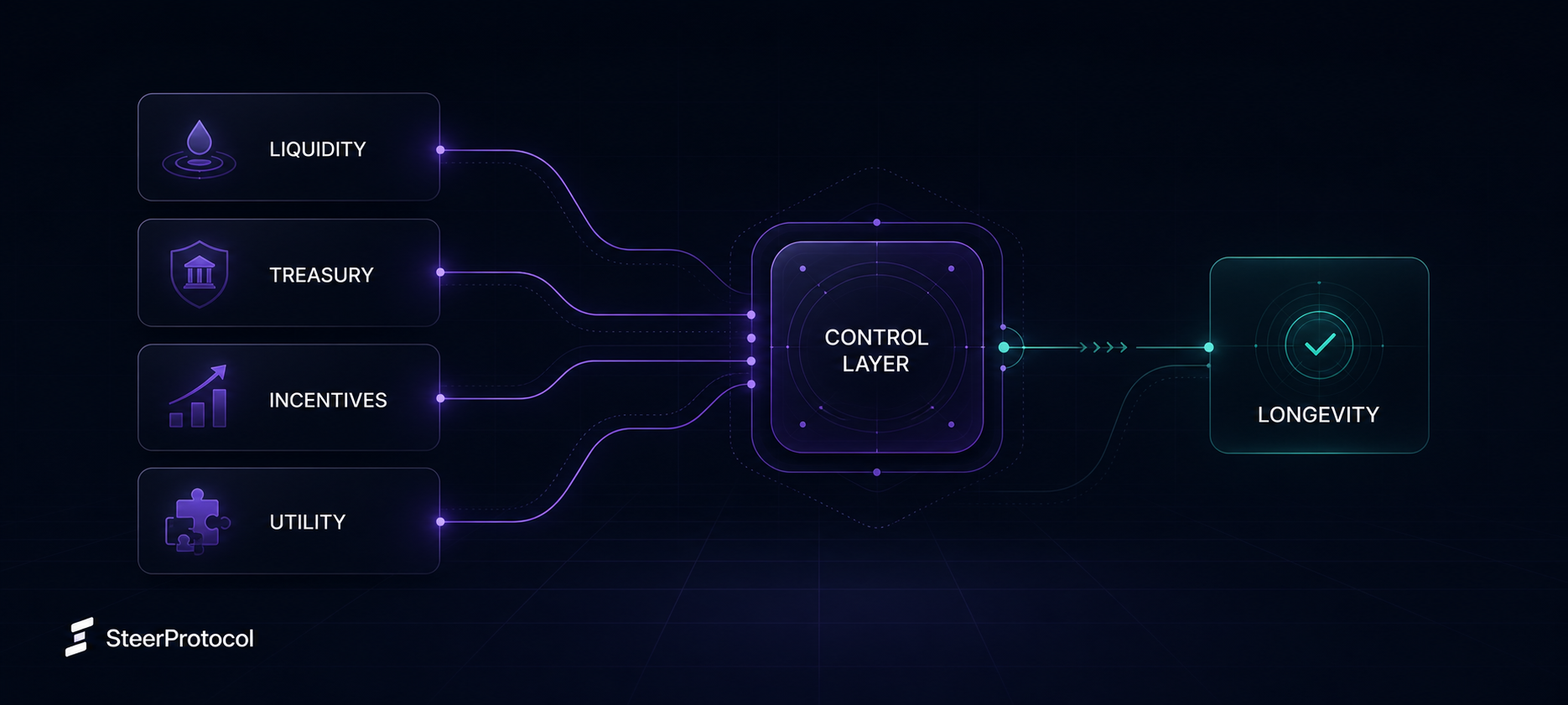

- Financialization — where the token becomes collateral, inventory, yield, or structured exposure.

- Control — where the ecosystem either owns the market’s core levers or cedes them to external intermediaries.

- Longevity — where the token either compounds into a durable system or becomes expensive to defend.

What happens at launch determines how much of that path remains open.

That is why token engineering and treasury management can no longer live in separate lanes.

They are not adjacent workstreams. They are two sides of the same system.

The old launch model is too fragmented

Historically, teams divided the work cleanly.

Token engineering handled supply, emissions, unlocks, listing coordination, market-maker agreements, and launch optics.

Treasury handled reserves, runway, protocol-owned liquidity, diversification, and post-launch market support.

In a simpler market, that split was manageable.

In a concentrated liquidity market, it becomes misleading.

Concentrated liquidity changed the structure of launch design. Uniswap v3 made liquidity far more capital-efficient by allowing LPs to concentrate capital inside specific price ranges. But that same design also means liquidity can become inactive or one-sided as soon as price exits the selected range.

Liquidity is no longer just a quantity question.

It is a behavior question.

A project can seed meaningful liquidity and still have a fragile market if that capital is placed poorly, moves out of range quickly, sits on the wrong venue, or cannot respond to volatility. Treasury can appear deployed while becoming inert precisely when the market needs it most.

That is the real blind spot in the old model.

It assumes token launch happens first and treasury starts mattering later.

In practice, treasury starts mattering the moment market structure becomes real.

This is the shift Steer has been building around. Across its broader footprint — 1,000+ tokens, 40+ chains, 4,000+ vaults, and 250+ strategic partners — the recurring lesson is clear: launches fail less from lack of capital than from fragmented design around how that capital is supposed to behave once the market goes live.

The real constraint is resource allocation under uncertainty

Teams do not usually separate token engineering from market formation because they misunderstand the theory.

They do it because they are operating under constraints.

They have limited treasury. Limited float. Limited exchange access. Limited market-maker bandwidth. Limited operational capacity. Limited time before launch. Limited confidence in what real demand will look like once the market goes live.

Under those constraints, projects optimize locally.

Some prioritize token engineering. They focus on supply discipline, vesting, unlock schedules, market-maker agreements, listings, and valuation optics. The assumption is that if the structure is clean enough, the market will form around it.

Others prioritize market formation. They focus on liquidity depth, venue mix, treasury deployment, onchain support, incentive design, and volatility absorption. The assumption is that if the market is healthy enough, token design can be stabilized later.

Both are rational responses to uncertainty.

Both are incomplete.

If token engineering dominates, the project may optimize for structure without giving the market enough capacity to absorb that structure. Supply can look disciplined on paper while liquidity is passive, treasury is reactive, and incentives are generic. The token becomes fragile the moment it meets volatility.

If market formation dominates without token discipline, the project may create early activity and visible depth, but without a credible supply path, emissions policy, or treasury framework. The market can look healthy at first and still become unstable as unlocks, treasury needs, or governance decisions begin hitting the system.

That is the deeper point:

Token engineering and market formation are not separate domains competing for attention. They are competing forces drawing from the same limited project resources.

If left unmanaged, each pulls the project toward its own failure mode.

The job is not to choose one.

The job is to temper both with the right instruments.

The market has punished the wrong assumptions

The last market cycle made one thing clear: many token launches did not fail only because they were poorly designed. They failed because they were designed around assumptions that looked rational in planning but broke under live market conditions.

One assumption was that high FDV and low float would signal quality.

In practice, markets increasingly read those structures as delayed dilution and future sell pressure.

Another assumption was that hype could substitute for demand.

Campaigns, airdrops, and incentives created attention, but often attracted sellers rather than durable users.

A third assumption was that CEX-led discovery could carry the market long enough for DeFi utility to emerge later.

But venue reality has changed. DEXs are no longer side venues. Onchain markets are now a meaningful part of primary market formation. The token’s first onchain liquidity, its first LP base, its first incentive structure, and its first DeFi integrations are no longer secondary concerns. They are part of the launch itself.

The lesson is not that launch teams were irrational.

It is that they were optimizing under uncertainty using assumptions the market no longer rewards.

Launch is where the lifecycle starts

The lifecycle does not begin after launch.

Launch is where the lifecycle starts.

The first market a token enters does more than set an opening price. It determines who controls price discovery, who captures volatility, whether liquidity is transparent or outsourced, and whether the token begins life inside DeFi or outside it.

That is why launch architecture matters.

A CEX-only launch can create immediate access and deeper early order books, but the formative market is shaped in a venue the issuer cannot fully observe or govern.

A DEX-only launch preserves transparency, programmability, and composability, but may begin with thinner depth and greater operational pressure on liquidity design.

A dual-track launch is often the strongest path because it separates distribution from control: centralized venues widen access, while onchain liquidity keeps the market composable, observable, and strategically governable from day one.

But dual-track design is not automatically the best of both worlds.

It only works when the tension between access and control is instrumented. Otherwise, it simply doubles complexity.

That is what path dependency means here.

The corridor set at TGE narrows the token’s future option set. A small deviation early can compound aggressively over time. One millimeter off center at launch can become a kilometer of divergence later.

If the first market externalizes control, fragments liquidity, or delays onchain utility, every later stage becomes harder.

If the first market is formed correctly, the token has a cleaner path from attention to liquidity, from liquidity to use, from use to financialization, and from there into durable control and longevity.

CEX and DEX are not just venues. They are competing market logics

Too many launch discussions still reduce venue strategy to a binary question: CEX or DEX?

That misses the actual issue.

CEX and DEX are not just venues. They are competing market logics. Each demands liquidity, inventory, incentives, treasury capacity, and operational focus.

A CEX-heavy path offers reach, immediate depth, and broader trader access. It can compress discovery into a tighter order-book environment and absorb some early volatility through professionalized liquidity. But it also moves the formative market into an environment the issuer does not fully control. Price discovery becomes more opaque. Treasury has fewer direct levers. Utility and composability are delayed. The token is distributed, but not yet deeply embedded in the onchain systems that can create durable demand.

A DEX-heavy path offers transparency, programmability, and immediate access to composability. The token begins life onchain, which shortens the path into LP participation, collateral usage, lending, structured products, and treasury-controlled market support. But it places more pressure on the issuer to get liquidity design, incentive routing, and automation right. Without active management, concentrated liquidity can become one-sided or inactive exactly when it is needed most. Without sticky incentives, LPs can disappear quickly. Without a treasury posture, volatility can overwhelm the market before utility has time to form.

This is why the best answer is rarely ideological.

It is usually some form of dual-track design.

But dual-track only works if the project knows what each side is supposed to do. CEX should not be treated as a substitute for onchain market structure. DEX should not be treated as a substitute for distribution. Each has a role. The launch architecture must make those roles explicit.

What imbalance looks like stage by stage

If path dependency is real, the most useful question is not whether CEX or DEX is better.

It is what happens when a project leans too far to one side too early.

A launch that is too CEX-heavy often looks strongest at the market-formation stage. Discovery is faster. Early depth is better. Visibility is higher. But the divergence appears later. Liquidity remains externally managed. Utility arrives slower because onchain composability is delayed. Financialization takes longer because the token was not born inside the systems that would naturally absorb it. Control weakens because the key early levers sit with exchanges and market makers rather than with the issuer and treasury.

Longevity then becomes dependent on maintaining external support rather than compounding internal utility.

A launch that is too DEX-heavy preserves the opposite strengths. Discovery is transparent. Composability starts earlier. The issuer keeps more direct control over liquidity and treasury behavior. But if that path is undercapitalized or under-instrumented, the divergence appears earlier. Discovery is weaker. Slippage is harsher. Liquidity can fragment. The token may fail to build enough stable depth for utility and financialization to emerge at the pace the project needs.

In this path, control may be preserved, but scale arrives too slowly or too violently.

A dual-track path preserves the most optionality, but only if it is actively designed. If not, it simply doubles the number of failure surfaces.

Liquidity quality decides whether the market holds

One of the most common launch mistakes is treating liquidity as a quantity problem.

In practice, it is a market-quality problem.

A token can launch with meaningful capital and still be structurally weak if that capital is sitting in the wrong places, becomes one-sided too quickly, or cannot respond when volatility expands.

In a concentrated liquidity market, passive liquidity can go out of range precisely when it is needed most. Treasury capital can sit idle while slippage rises. A market can look funded and still be fragile.

So the real question is not how much liquidity is seeded.

It is what that liquidity is supposed to do.

Is it there for price discovery? Tighter execution? Treasury distribution? Volatility absorption? A downside backstop? Cross-chain parity? Incentive efficiency? Market depth while utility develops?

These are not purely tokenomics questions.

They are not purely treasury questions either.

They are both.

This is where Steer’s operating model becomes relevant. Smart Pools, treasury-aware ALM, and Dynamic Rebalance are built around a simple idea: liquidity should not behave like a static deposit. It should behave like policy.

Liquidity should be able to express intent. It should know whether it is optimizing for depth, fees, inventory balance, volatility response, treasury protection, or ecosystem growth.

That is why liquidity quality is where treasury posture becomes visible in the market.

The failure modes of separation are already familiar

When token engineering is handled separately from treasury and market formation, the failure patterns are usually obvious.

The first is the passive CLMM trap. Liquidity is technically deployed, but once price moves, capital goes out of range, becomes one-sided, and stops doing the job the project assumed it would do. Treasury appears present, but becomes inert when the market needs support.

The second is inactive protocol-owned liquidity. Teams seed pools and assume they have built market support, but the capital is not positioned correctly, segmented by objective, or actively managed. The treasury is in the market, but it is not functioning as policy.

The third is manual panic. Teams try to manage fast onchain markets with slow human intervention. By the time they notice slippage, range drift, or inventory imbalance, the market has already moved.

The fourth is the mercenary incentive cycle. Generic APY attracts temporary participation, but because incentives are not attached to market-quality outcomes, the liquidity does not stay. Emissions are spent, but resilience is not built.

The fifth is the treasury reflex loop. As price weakens, treasury flexibility weakens. As treasury becomes more reactive, market quality deteriorates further. Once that reflex begins, the cost of stabilization rises quickly.

These are not edge cases.

They are what happens when launch structure and market support are designed as separate systems.

Utility does not appear on its own

A token does not become durable just because it becomes tradable.

The next transition is whether it becomes usable.

This is where the token starts being paired, held, deposited, collateralized, staked, routed through strategies, or embedded into actual onchain behavior. It is where demand stops being purely speculative and starts becoming functional.

Liquidity creates the conditions for use, but it does not create use by itself.

This is where launch path starts compounding.

A token that forms mainly in centralized venues often has to rebuild its onchain presence later. It must recover composability after the market has already formed somewhere else.

A token launched with credible onchain liquidity from day one is already living where DeFi can use it. That shortens the path from speculation to integration.

This is also where incentive design matters more than most teams expect.

If incentives are designed around generic APY and mercenary farming, they can inflate TVL without creating lasting market quality. If they are designed around depth, retention, range quality, liquidity uptime, wallet diversity, or specific market-health outcomes, they help the token move from being merely traded to being productively used.

That is why liquidity and incentives should not be treated as separate modules.

The value question at this stage is simple:

Does the token become productive capital, or does it remain mostly an object of trade?

A token becomes more valuable when it becomes financeable

The next step in the lifecycle is not more trading.

It is financialization.

This is where the token becomes part of a broader capital stack: lending, leverage, structured yield, treasury sleeves, hedged inventory, volatility products, or more advanced financial strategies.

Once that happens, the token stops being only a spot instrument. It becomes capital that can be deployed, transformed, collateralized, and layered into other products.

This is the stage where a token stops being just an asset and starts becoming the base layer for a product system.

The current DeFi market is already large enough to support that transition. Large lending markets, deep stablecoin liquidity, and increasingly sophisticated onchain venues create the conditions for liquid assets to become financeable assets.

That means the question is no longer whether a token can trade.

The question is whether it can become usable inside the financial system around it.

This is also where programmable liquidity becomes more than an execution tool.

A generic LP framework can provide market presence.

A programmable liquidity framework can express a market thesis.

Dynamic Rebalance is a useful example of that shift. By controlling placement mode, range width, liquidity shape, and rebalance triggers, different token markets can express different inventory postures and different responses to volatility. That is not just better execution. It is a broader control layer for how a token market should behave as it matures.

The real question is who controls the market you built

At some point, every token market reveals who is actually in control.

Control is not just governance votes.

It shows up earlier: who shapes price discovery, who captures volatility, who can intervene when liquidity weakens, and whether the ecosystem owns the system dynamics or merely participates in them.

This is where control stops being theoretical.

Liquidity ownership, policy enforcement, and strategy execution determine whether value accrues to the ecosystem or to external intermediaries.

A CEX-centered path often cedes those levers to exchanges and market makers. A DEX-native or properly designed dual-track path preserves more room for policy, programmability, and strategic response.

This is why market design is governance before governance.

A team does not control a token market just because it launched the token. It controls the market only if it still has meaningful levers over liquidity behavior, treasury deployment, and incentive outcomes after trading begins.

Longevity is not post-launch maintenance

By the time teams start worrying about long-term value, most of the structural work has already been done.

Longevity does not appear at the end by itself. It is the cumulative outcome of whether the earlier stages were designed correctly.

If the first market is weak, liquidity stays fragile.

If liquidity stays fragile, utility stays thin.

If utility stays thin, financeability remains limited.

If financeability remains limited, control weakens.

And if control weakens, longevity becomes expensive to defend.

This is where treasury management matters most.

The post-TGE problem is not just a pool problem. It is a treasury portfolio problem. Treasury needs policy-driven sleeves for market health, diversification, growth, and defense. It cannot be treated as a wallet plus a pool.

Without that structure, teams fall into the classic reflexive loop:

Sell treasury tokens to fund operations. Price weakens. Liquidity worsens. Market confidence drops. Treasury flexibility shrinks. More selling pressure appears.

Once that loop starts, stabilization becomes more expensive with every cycle.

That is why treasury management does not belong after launch.

It belongs inside lifecycle design from the beginning.

A better launch architecture is integrated

If token engineering and treasury management are designed together, the entire launch architecture changes.

Before launch, the team defines what kind of market it is trying to build:

- discovery-heavy,

- stability-oriented,

- treasury-distributive,

- backstop-first,

- utility-led,

- or dual-track with explicit access and control objectives.

Liquidity is then deployed with specific jobs, not just seeded.

Venue mix is chosen for both reach and control.

Protocol-owned liquidity is treated as strategic inventory, not passive capital.

Incentives are routed toward desired behavior, not generic TVL.

Treasury sleeves are designed around market health, runway, defense, growth, and future financialization.

And once the market goes live, automation handles the parts that humans are too slow and inconsistent to manage manually.

This is the operating model Steer has been pushing toward: Smart Pools for automated liquidity execution, Smart Rewards for aligned incentive routing, and Dynamic Rebalance for programmable liquidity logic that can adapt to the market being served.

The point is not automation for its own sake.

The point is making token policy and treasury policy executable inside market structure.

That is what a unified token-treasury architecture looks like.

Not launch first and treasury later.

One system from day one.

Conclusion: TGE is market formation under constraints

The most useful way to think about TGE is not token distribution. It is market formation under constraints.

And those constraints are not abstract. They are limited treasury, limited float, limited exchange access, limited operational bandwidth, and imperfect assumptions about how real demand will behave once the token goes live.

That is why the lifecycle is path dependent.

Launch structure shapes liquidity quality. Liquidity quality shapes use.

Use shapes financialization. Financialization shapes control.

Control shapes longevity.

Once the market begins on the wrong footing, every later stage becomes harder to recover.

So the practical conclusion is straightforward:

Token engineering and treasury management must converge before TGE, not after it. Because if the market is formed incorrectly, the lifecycle narrows fast. But if the market is formed correctly, the token has a real path to become more than a trade.

It can become usable capital.

It can become financeable capital.

And eventually, it can become a durable market system.

Recent Insights and Updates

Expand your knowledge with these hand-picked articles, tailored to keep you ahead in the space.

.avif)